By Izak Odendaal and Dave Mohr, Old Mutual Wealth

The continued rapid spread of the Wuhan coronavirus – which goes by the technical name of 2019-nCov – is still dominating the headlines, and markets have predictably been under pressure over the past few weeks. This raises a number of important questions, including how we should think about potentially disastrous events in an investment context.

The continued rapid spread of the Wuhan coronavirus – which goes by the technical name of 2019-nCov – is still dominating the headlines, and markets have predictably been under pressure over the past few weeks. This raises a number of important questions, including how we should think about potentially disastrous events in an investment context.

But first, what do we know so far? Despite the World Health Organisation labelling it a global health emergency, most of the infections and all the deaths from the pneumonia-like virus have so far been contained to China. More people have now been infected than in the 2003 SARS outbreak, but fewer have died ‒ about 2% of those infected. There is often an inverse relationship between how quickly a disease spreads and how deadly it is. This makes sense, since a virus tends to need live bodies to host and spread it.

The Chinese government has acted with speed to contain the spread of the virus and treat patients. A hospital has already been built within two weeks, something that can only happen in China. Whole cities have been quarantined. This is clearly hugely disruptive and will knock first-quarter economic growth in China.

The Chinese government has acted with speed to contain the spread of the virus and treat patients. A hospital has already been built within two weeks, something that can only happen in China. Whole cities have been quarantined. This is clearly hugely disruptive and will knock first-quarter economic growth in China.

Some foreign airlines have cancelled flights in and out of China and multinationals have been pulling staff. The Lunar New Year is peak travel season in China and the tourism industry and associated sectors will be deeply affected. Surrounding countries in Asia are also big beneficiaries of Chinese tourist spending. China is a much bigger part of the global economy today compared to 2003. Its own economy has also shifted away from a focus on manufacturing to consumption and services. The economic impact of the 2019-nCov might therefore be worse than SARS in 2003, even if the virus is less deadly.

Some perspective is needed. The US Centres for Disease Control estimate that seasonal influenza annually hospitalises 210 000 people in America, leading to 61 000 deaths. Worldwide, it estimates 646 000 annual deaths. In other words, there are always diseases that take a toll on economic activity. The negative economic impact from the coronavirus is therefore not the scale of death or hospitalisation, but rather the disruption to economic activity as a result of the precautions taken to halt its spread.

The outbreak of the virus was an unexpected shock to the Chinese economy, but if the contagion is contained, the fear will fade and economic activity will resume.

Some lost activity can be made up, some not. Unfilled factory orders can be delivered late, but people aren’t going to buy two lunches today because they couldn’t buy one yesterday (the same logic applies to local load-shedding, which has resumed after a pleasant hiatus).

Black swan swoon

Apart from the coronavirus, the increased attention on global warming and rising Middle Eastern tensions have brought the idea of catastrophe to the fore again. How should we think about cataclysmic events and investing more broadly?

The first point is if things truly go wrong, such as a global nuclear apocalypse, the value of your portfolio might be the furthest thing from your mind.

There is always uncertainty when investing for the simple reason that we cannot predict the future. We can make educated guesses (otherwise known as forecasting), but will never have absolute certainty. However, known risks tend to be priced in already (such as a likely Moody’s downgrade), but it is when unknown risks materialise that market mayhem ensues. As a former US Defence Secretary infamously said in the context of the Iraqi weapons of mass destruction they never found: “There are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns ‒ the ones we don’t know we don’t know… it is the latter category that tend to be the difficult ones.” These unknown unknowns are known as “tail risks” or “black swans” in investing jargon: low-probability events with potentially disastrous consequences.

In modern investing history, there have been only a few external events that have wiped investors out. Investors were more likely to face ruin from government policies (such as those that lead to hyperinflation) than from war, diseases or natural disasters.

The biggest killer, though, is investor behaviour: buying high and selling low, reckless borrowing and excessive optimism. The 9/11 attacks, the biggest geopolitical shock of the past 30 years, caused a short-lived wobble on financial markets. Getting sucked into the dotcom bubble a few years earlier would have had a far worse portfolio impact. And of course, subprime American home loans – sliced, diced, repackaged, levered up and sold to unsuspecting investors – nearly caused a collapse of global capitalism eight years later.

The last truly devastating global pandemic was the Spanish flu of 1918, but since it happened towards the end of the First World War (indeed, the mass mobilisation and movement of troops helped spread the virus) it is hard to disentangle its economic impact from that of the war. It is estimated to have killed more people than the battlefields. South Africa was particularly hard hit, with some 500 000 succumbing to the virus.

The two World Wars caused untold human and physical destruction, but not all portfolios were wiped out. Some investments still did well. The US market bottomed in 1942, shortly before the country entered the war, and continued the surge ahead in the years after. Needless to say, German and Japanese equity markets lost 90% of their values during the war. South African equities returned 80% in real terms between 1940 and 1945.

The largest loss of private wealth in a single country in modern history was probably the 1917 Russian revolution, which abolished all private ownership. The only way to preserve wealth was to flee the country with all your possessions in tow.

Diversification still the best defence

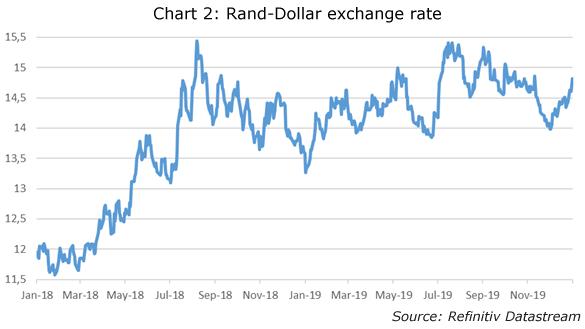

Apart from the relatively small asset class of catastrophe bonds (which pay out when something really bad but specific happens, like a hurricane), the best defence we have is diversification. The dollar is still the world’s ultimate safe haven. It rallied in January amid rising risk aversion and the rand weakened. While equity markets have sold off everywhere in response to the coronavirus fears, global equities were still positive in rand terms in January due to the weaker currency.

Geographic diversification is important, because natural disasters, disease outbreaks and even wars tend to be regional. As it happens, South African investors have a lot of exposure to Chinese consumer spending through shares like Naspers and Richemont, and to Chinese industrial activity through the big commodity exporters. Local equities have therefore been hit by the coronavirus.

Many consider gold the ultimate safe-haven investment. However, it appears to respond more to fears of inflation than anything else. It only jumped 7% on the 9/11 attacks and gave back those gains in a month. Gold fell during most of the 2008 Global Financial Crisis. Its all-time 2011 peak of $1 800 coincided with fears that quantitative easing would lead to runaway inflation. That never happened; on the contrary inflation has been persistently and frustratingly low (from the point of view of central bankers) ever since. Gold is at the highest level since 2013, but still 20% below its peak.

Global warming

Climate change, which is really a euphemism for global warming, presents a new problem for investors that is rightly getting a lot of attention. The timelines over which global warming scenarios could play out are highly uncertain, but it is important to start thinking about the implications.

Broadly speaking, there are three risks to portfolios: an unstable climate can lead to more disasters (such as hurricanes, floods and bushfires), disrupting economic activity and leading to huge insurance losses. This is negative for equities. Governments might have to borrow more to respond to such events, potentially putting upward pressure on interest rates.

Secondly, some areas might become undeliverable due to rising sea levels or persistent droughts, leading to real estate assets losing value. The displacement of people from these areas can cause disruption elsewhere.

Thirdly, as consumption patterns and regulations change in response to climate change, it could lead to ‘stranded assets’. Factories, coal mines and oil wells could become worthless. However, other mines could become more valuable if they produce commodities needed for the technologies that can tackle global warming, including renewable energy.

These technologies present a huge investment opportunity. Despite our ability to hurt each other and damage our planet, it has never paid to bet against human ingenuity in the long run.

Volatility is normal

Back to the present, financial markets are always volatile in the short term. However, over the longer term, equity prices move to reflect company earnings, property prices reflect rental growth and bonds respond to the inflation outlook. It is these real variables that we should pay most attention to, not the events that grab headlines. Until such time as there is clarity on how those headline-grabbing events, such as the coronavirus, will impact those real variables, portfolio tinkering is unwise. Rather, portfolios should be appropriately diversified at the outset.

History also shows that most of these events have a short-lived impact on markets and the best approach is to be patient and sit tight.

Greetings

I m interested in buying shares during this pandemic

What advice would you give me and which companies that are offering shares at the moment and how one can get them

This is not the time to take risks. So if you have never invested directly in shares, then this is not the time to start as it requires experience and knowledge. Also do not lock money into investments if you are worried about future income. If you want to start investing it is best to start with unit trusts or exchange traded funds that give you diversification

Hi Maya

We currently live in Canada and have a large sum of cash still sitting in SA.

With the recent tank in the exchange rate, bringing it over at the current rate will mean a huge loss to money that is ultimately needed to buy a home here.

I’m wondering if you could offer advice on where and how to best invest our savings in SA? We don’t need the cash at the moment and could wait 12-18 months or more before we buy here.

Many thanks,

YP

Check out RSA Retail Bonds – one of the best interest rates. I see they are not accepting new funds during lock down, but hopefully that will end https://secure.rsaretailbonds.gov.za/Home.aspx

Otherwise look at what the bank is offering for a 18 month fixed deposit

Hi there,

We have been applying to consolidate our loans and borrow more money to build a new family home.

Is this now too risky now given all the talk of a recession happening soon?

I don’t know what to do.

What is the advice around borrowing / lending at the moment?

Many thanks,

TR

I think you need to look at your own situation and assess the risks to your income. perhaps go ahead with the consolidation but do not draw on the funds until you have more certainty